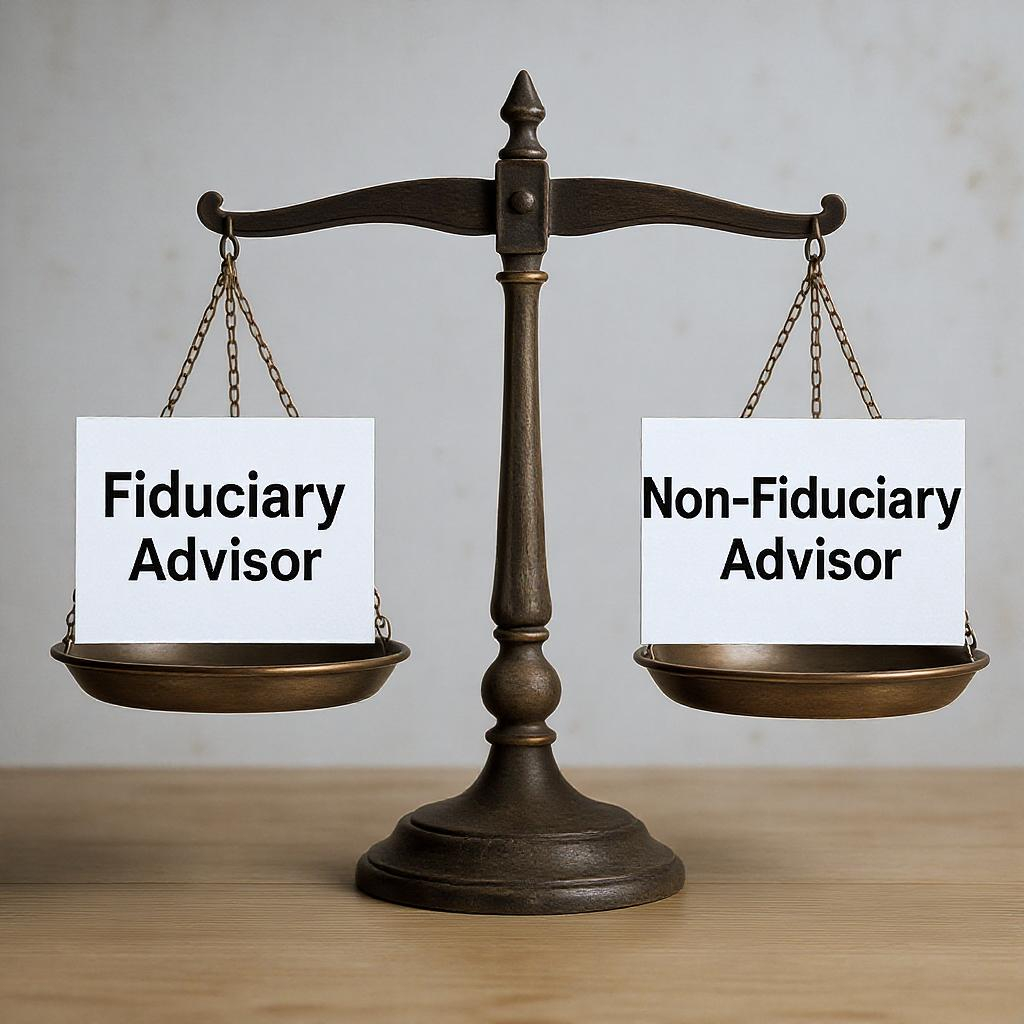

Let’s talk about your money—your savings, your retirement goals, your children’s education. All of it depends on the financial choices you make. And when it comes to advice on those choices, the real question is: who do you trust?

This isn’t just a small detail. It’s the difference between guidance that’s tailored to you and recommendations that may serve someone else’s interests. At the heart of it all is one essential question: Is your advisor a fiduciary?

If you’re not sure what that means—or why it matters—it’s time to find out. Because knowing the answer could be the most important step you take toward protecting your financial future.