Amid the historic surge in S&P 500 valuations, reaching new highs in October 2025, investors face a complex landscape marked by both optimism and heightened risk. At Vistamark Investments, the current environment underscores the value of blending opportunities in public market equities with strategic allocations to private equity and private credit. These alternative assets enhance portfolio diversification, offer higher expected risk-adjusted returns, and provide income stability essential for navigating ongoing volatility and economic shifts. With central banks adapting monetary policy and fiscal challenges ongoing, adopting a multi-asset, globally diversified approach anchored by rigorous risk management remains key to building resilient portfolios and securing enduring wealth.

Historic Valuations and Market Context

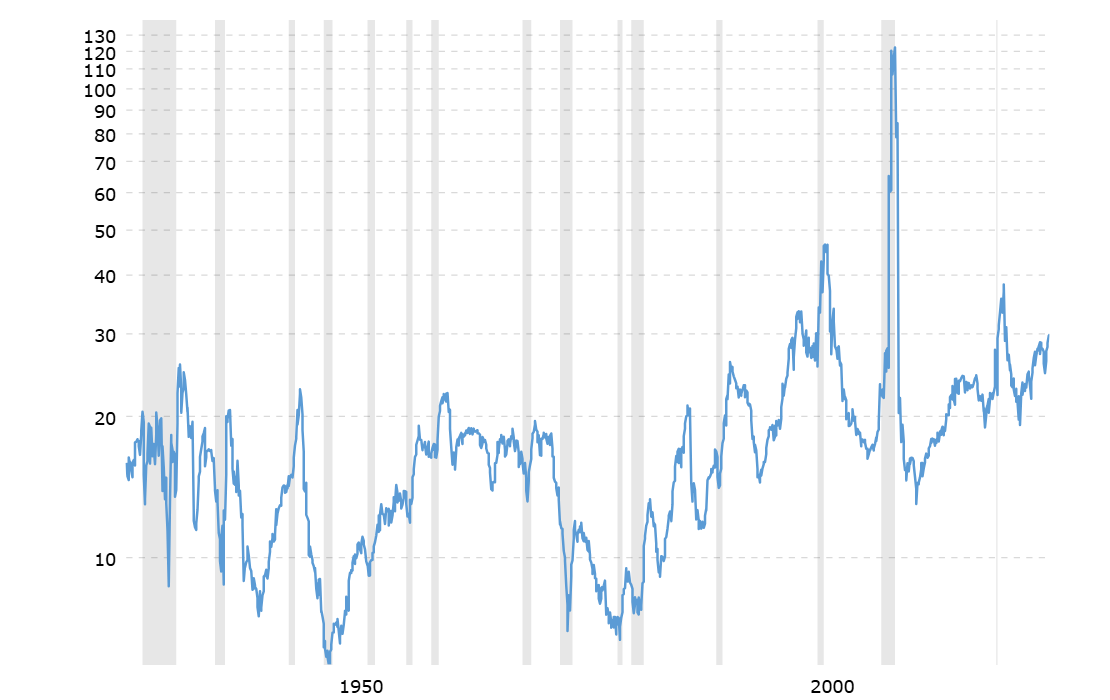

The S&P 500’s price-to-earnings (P/E) ratio, historically ranging between 15 and 20 over market cycles, now exceeds 30—levels only experienced during rare peaks such as the 2009 financial crisis and the height of the dot-com bubble in 1999–2000. During the dot-com era, the index maintained P/E ratios around 30–32. The only period with higher P/Es was March 2009, when the ratio briefly spiked above 120 due to a dramatic temporary earnings collapse. In October 2025, the S&P 500 P/E sits near 31, virtually matching its highest sustained pre-crisis readings of the last 50 years, and well above the long-term average of around 18.

Importantly, some of these historical valuation peaks have occurred at market bottoms rather than tops, as a result of collapsing earnings during recessions or crises rather than high prices. For example, the extraordinary P/E spike in 2008–2009 was driven largely by a sharp decline in corporate profits, not exuberant valuations. High P/E ratios in these periods often signal distressed earnings environments, not purely investor exuberance. This distinction is critical for interpreting the true implications of today’s elevated valuations.

Historical P/E Ratios

Source: Macrotrends

The Challenge of Market Timing

High market valuations can persist—sometimes much longer than investors expect. For example, valuations remained elevated for several years in the late 1990s, with markets becoming even more highly valued from 1997 until the dot-com bust in 2000. Other examples include long bull runs in the 1980s and 2010s where expensive markets became even more expensive before eventual corrections. It is difficult to predict with precision when a bear market will arrive; many respected analysts and investors have called for downturns years before they materialized—or missed rallies entirely.

A classic investing joke captures this reality: “One brilliant investor accurately predicted six out of the last three bear markets.” In other words, market experts often foresee trouble that doesn't arrive, or comes much later than anticipated. Rather than relying on market timing, disciplined investing, diversification, and a long-term perspective have proven to be far more effective for building wealth.

These current conditions indicate one of the most expensive markets on record—apart from short-lived crisis distortions—and suggest a starting point from which forward returns have historically been muted. Past performance is no guarantee of future results.

As of late 2025, despite earnings growth estimates near 10.6%, the potential for heightened volatility and valuation repricing persists. Investors should heed these signals as they seek to preserve capital and capitalize on opportunities, balancing exposure between public equity markets and alternative investments.

Why Pivot Toward Private Equity and Private Credit?

Vistamark’s approach increasingly favors private equity and private credit as vital components of portfolio construction amid expensive public equities. Historically, private equity has outperformed public markets over long horizons, driven by active management and operational improvements that create compounding growth. Please note, past performance is no guarantee of future results.

Leading institutional investors, as reported by Private Equity International’s Global Investor Ranking (2025) and Nuveen’s Fifth Annual EQuilibrium Global Institutional Investor Survey, typically target 20–30% allocations to private equity and private credit, with major institutions such as Temasek Holdings, GIC Private Limited, CPP Investments, and Mubadala all reporting substantial exposures. These allocations are designed to capture expected diversification benefits and expected inflation-beating returns while helping to mitigate stock market swings.

Private credit complements private equity by offering steady income, floating-rate exposure, and reduced volatility through contractual cash flows, which are particularly valuable amid rising rates and inflationary pressures. The retreat of traditional banks from middle-market lending has expanded expected private credit opportunities. Again, it’s important to remember that past performance does not predict future returns. The expected illiquidity premium typical of private markets also cushions portfolios against public market shocks.

Resilience During Bear Markets

Private equity and private credit tend to exhibit greater expected resilience during bear markets and economic downturns due to several factors.

The illiquidity and valuation lag of private equity dampen short-term market swings, as these assets are not marked to market daily.

Active management by private equity firms drives operational improvements and strategic pivots that help portfolio companies weather economic storms. Their access to capital during stress periods provides an important lifeline.

Private credit benefits from contractual cash flows and structural protections like covenants, ensuring expected income stability even during volatility.

Moreover, private markets generally show lower correlation to public market sentiment, reducing price sensitivity to market panics.

Finally, downturns present opportunities for private equity to acquire undervalued assets, positioning portfolios for expected outsized gains in recoveries.

These combined features make private equity and private credit powerful tools for expected diversification and risk mitigation in turbulent markets.

The Vistamark Investment Philosophy

At Vistamark Investments, disciplined overweight allocations to private equity and private credit reflect a commitment to building resilient, long-term wealth. Private equity investments target durable growth through operational value creation and venture backing in innovation sectors. Private credit serves as a volatility buffer and reliable income source, aligning with our outlook on inflation and interest rate dynamics.

Our portfolio framework combines access to top-tier alternative managers, rigorous due diligence, and a balance of liquid and illiquid exposures to optimize expected risk-adjusted returns. This multi-asset strategy enhances expected diversification beyond traditional stocks and bonds, preparing investors to navigate market uncertainties and capitalize on global growth themes. It is always essential to remember that historical returns do not guarantee future results.

Conclusion

With the S&P 500 trading at valuation levels rarely seen outside the dot-com bubble—and with current P/E ratios matching only a handful of brief, extraordinary periods in the last half-century—embracing meaningful allocations to private equity and private credit is a prudent strategy for those seeking wealth preservation and growth. These alternative assets provide essential expected diversification, expected income stability, and the potential for superior expected returns, all crucial in today’s dynamic and uncertain investment landscape. However, no investment strategy can guarantee future performance, and all investments involve risk, including possible loss of principal. Combining public market insights with a thoughtful, multi-asset approach anchored in disciplined risk management positions investors to thrive amid evolving market conditions and secure enduring financial resilience.

For more information and personalized guidance, please feel free to reach out to Vistamark Investments LLC. You can contact us at

312-895-3001, visit our website at

www.vistamarkllc.com, or send us an email to

info@vistamarkllc.com.